The Facts About Mortgage Investment Corporation Revealed

Table of ContentsThe Of Mortgage Investment CorporationThe 15-Second Trick For Mortgage Investment CorporationMortgage Investment Corporation Things To Know Before You BuyMortgage Investment Corporation Fundamentals Explained3 Easy Facts About Mortgage Investment Corporation Described

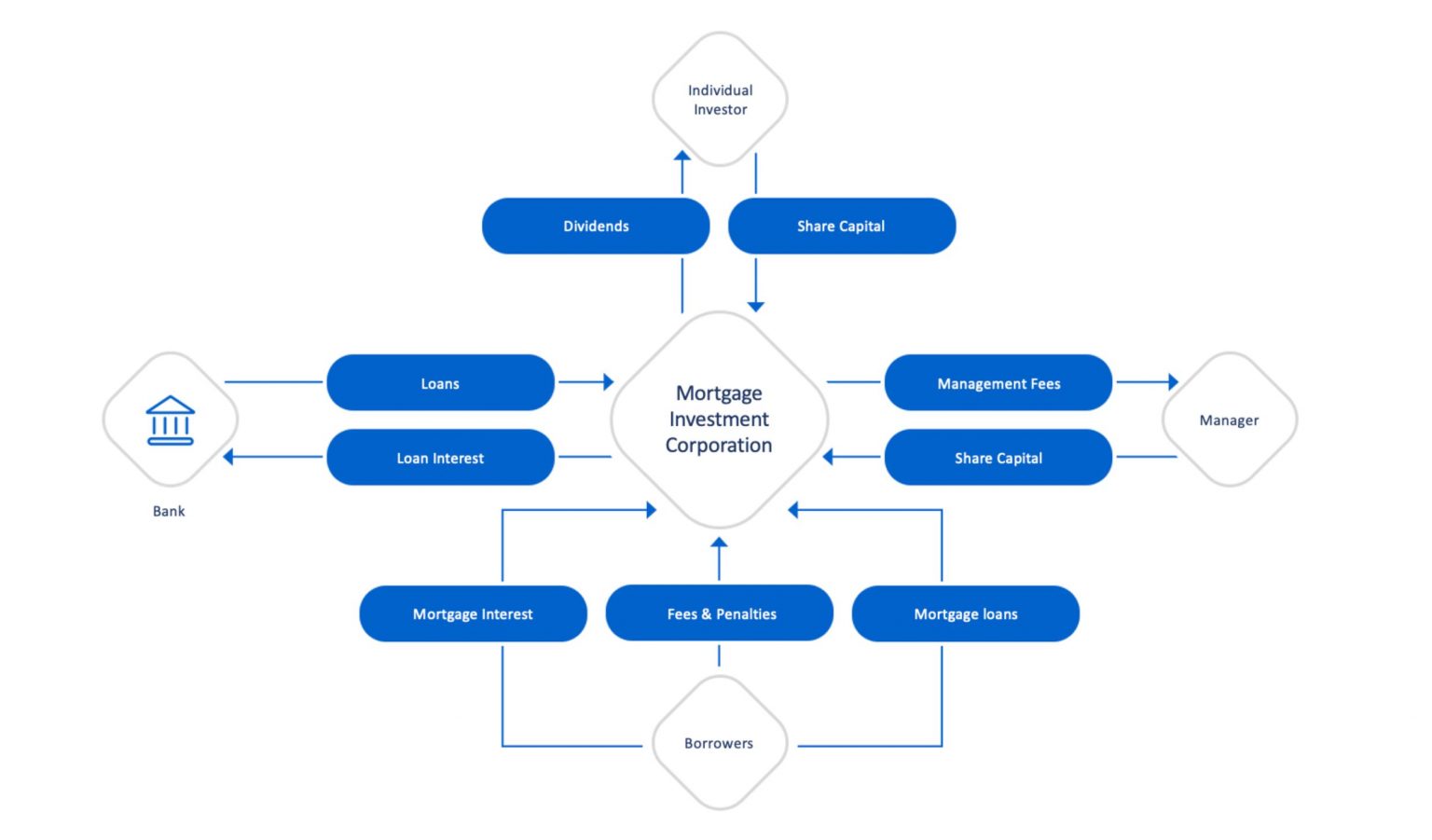

Does the MICs credit report committee review each home loan? In most scenarios, home mortgage brokers manage MICs. The broker needs to not work as a member of the credit rating board, as this puts him/her in a direct problem of interest considered that brokers normally gain a payment for placing the mortgages. 3. Do the supervisors, members of credit history committee and fund manager have their very own funds spent? Although a yes to this inquiry does not supply a risk-free investment, it must give some increased protection if assessed along with various other sensible borrowing policies.Is the MIC levered? The financial establishment will accept certain mortgages owned by the MIC as safety for a line of credit rating.

The Definitive Guide for Mortgage Investment Corporation

Last updated: Nov (Mortgage Investment Corporation). 14, 2018 Few investments couple of financial investments advantageous as helpful Mortgage Investment Home mortgage Financial InvestmentMIC), when it comes to returns and tax benefitsTax obligation Due to the fact that of their corporate structure, MICs do not pay revenue tax and are legitimately mandated to distribute all of their earnings to investors.

This does not mean there are not threats, but, generally talking, whatever the broader stock market is doing, the Canadian real estate market, particularly significant metropolitan locations like Toronto, Vancouver, and Montreal executes well. A MIC is a firm developed under the guidelines lay out in the Earnings Tax Act, Section 130.1.

The MIC makes income from those home loans on rate of interest costs and general costs. The real allure of a Home mortgage Financial Investment Company is the yield it supplies financiers contrasted to other set revenue investments - Mortgage Investment Corporation. You will certainly have no difficulty locating a GIC that pays 2% for an one-year term, as federal government bonds are similarly as reduced

Mortgage Investment Corporation - Truths

There are rigorous requirements under the Earnings Tax Obligation Act that a firm should fulfill before it certifies as a MIC. A MIC should be a Canadian company and it should invest its funds in mortgages. MICs are not permitted to handle or develop actual estate home. That stated, there are times when the MIC winds up having the mortgaged building as a result of repossession, sale arrangement, etc.

MICs issue typical and preferred shares, releasing visit this website redeemable preferred shares to investors with a dealt with reward rate. Most of the times, these shares are considered to be "certified investments" for deferred earnings strategies. Mortgage Investment Corporation. This is suitable for financiers that purchase Home loan Financial investment Company shares with a self-directed licensed retirement cost savings strategy (RRSP), registered retired life earnings fund (RRIF), tax-free financial savings account (TFSA), deferred profit-sharing strategy (DPSP), signed up education savings plan (RESP), or signed up disability cost savings strategy (RDSP)

Some Known Incorrect Statements About Mortgage Investment Corporation

And Deferred Strategies do not pay any kind of tax obligation additional resources on the rate of interest they are approximated to obtain. That claimed, those that hold TFSAs and annuitants of RRSPs or RRIFs might be struck with particular penalty taxes if the investment in the MIC is thought about to be a "forbidden investment" according to copyright's tax code.

They will guarantee you have actually located a Home mortgage Financial investment Company with "qualified investment" condition. If the MIC qualifies, maybe really helpful come tax obligation time since the MIC does not pay tax on the passion earnings and neither does the Deferred Strategy. Much more broadly, if the MIC fails to meet the demands set out by the Income Tax Act, the MICs revenue will certainly be taxed prior to it gets dispersed to investors, decreasing returns considerably.

A lot of these risks can be minimized though by talking with a tax obligation professional and financial investment rep. FBC has actually functioned exclusively with Canadian small company owners, business owners, capitalists, ranch useful site operators, and independent professionals for over 65 years. Over that time, we have aided 10s of countless customers from across the country prepare and file their tax obligations.

Some Known Factual Statements About Mortgage Investment Corporation

It shows up both the genuine estate and stock exchange in copyright go to all time highs Meanwhile returns on bonds and GICs are still near record lows. Also cash money is losing its appeal due to the fact that energy and food rates have pushed the rising cost of living price to a multi-year high. Which begs the concern: Where can we still locate value? Well I believe I have the answer! In May I blogged concerning considering home mortgage investment companies.

If rates of interest climb, a MIC's return would likewise boost because higher home mortgage prices mean more revenue! Individuals who buy a home mortgage financial investment corporation do not own the property. MIC investors just earn money from the excellent placement of being a lender! It's like peer to peer borrowing in the U.S., Estonia, or other parts of Europe, except every finance in a MIC is safeguarded by real estate.

Many tough working Canadians that desire to purchase a house can not get home mortgages from typical financial institutions due to the fact that probably they're self utilized, or don't have an established credit history. Or maybe they desire a short term finance to establish a large building or make some improvements. Banks tend to overlook these prospective borrowers due to the fact that self used Canadians don't have secure earnings.